乐居财经讯 李礼 2月7日,华创证券发布万科 A(000002)2020 年 1 月销售数据点评。

事件:

万科公布公司 1 月销售数据,1 月公司实现签约金额 549.1 亿元,同比增长12.3%;实现签约面积 333.5 万平方米,同比增长 5%。1 月公司新增建面 69.7万平方米,同比下降 76.5%;总地价 38.2 亿元,同比下降 70.6%。

点评:

1 月销售 549 亿、同比+12%,预计今年销售平稳

1 月公司实现签约金额 549.1 亿元,环比下降 4.2%、同比增长 12.3%;实现签约面积 333.5 万平方米,环比下降 19.6%、同比增长 5%;销售均价 16,465 元/平,环比增长 19.2%、同比增长 7%。公司单月销售金额居克而瑞榜单第一。我们认为,近期受到新冠肺炎疫情的持续扩散影响,一季度房地产市场成交压力或将延续,甚至对全年销售形成负面影响,但购房需求只是延后、并非消失,同时一季度占比较小,预计总体销售负面影响可控;与此同时,新冠肺炎疫情也将使得经济和财政压力进一步加大,也将打破政府兼顾控地产和稳经济的弱平衡,或将促发逆周期调控弹性进一步加大。此外,在一二线市场销售平稳以及宝万股权之争即将落幕的背景下,预计公司 2020 年的销售或将平稳增长。

1 月拿地 38 亿元、拿地谨慎,拿地额/销售额为 7%

1 月公司在土地市场获取上海、南通、太原等地 6 个项目,拿地区域主要集中于一二线城市及环都市圈。1 月公司新增建面 69.7 万平方米,环比下降 42.8%、同比下降 76.5%;对应总地价 38.2 亿元,环比下降 67.4%,拿地金额占比销售金额达 7%,较 2019 年的 37%下降 30pct,拿地谨慎由于疫情和春节影响;平均楼面价 5,482 元/平米,环比下降 43.1%;拿地面积占比销售面积 21%,较2019 年的 99%下降 78pct;拿地均价占比当月销售均价 33.3%,较 2019 年的37.8%下降 4pct。按销售均价 1.65 万元/平估算公司 1-1 月累计新增货值 115 亿元,低于同期销售金额 549 亿元,拿地仍较谨慎。

投资建议:全年销售平稳,股权之争落幕在即,维持“强推”评级

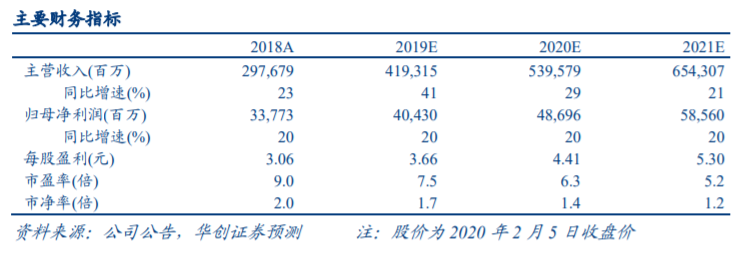

万科作为行业三十载领跑者,在提前倡导高周转、探索住宅工业化、专注中小户型精装修产品、领先建立三级管控架构、布局三大城市群、实施多项人才计划、深化小股操盘模式以及创新业务发展等方面都是当之无愧的先行者,其成果也已体现在公司过去 10 年的销售和业绩双双高增中,也体现在行业领先的稳健经营和财务指标中。而面向未来,在本轮房地产小周期延长的反常周期中,万科在住宅开发行业将继续保持龙头优势,同时公司在物业服务、商业地产、物流地产、长租公寓、养老地产和轨道物业等细分领域也已领跑行业,未来业绩和估值的贡献值得期待。我们维持公司 2019-21 年每股收益预测分别为 3.66、4.41、5.30 元,维持“强推”评级。

风险提示:新冠肺炎疫情影响超预期、房地产调控和融资政策超预期收紧。

更多精彩內容,請登陸

財華香港網 (https://www.finet.hk/)

現代電視 (http://www.fintv.com)