乐居财经讯 李礼 2月12日,天风证券发布中南建设研报。

事件:中南建设发布 2020 年 1 月份经营情况公告,2020 年 1 月公司实现合同销售面积 45.7 万平方米,较去年同比下降 35%,合同销售金额 59.5 亿元,同比减少 32%。

点评:

销售规模短暂下滑,均价有所提升。2020 年 1 月公司实现合同销售面积 45.7 万平方米,销售金额 59.5 亿元,同比分别下降 35%、32%;增速较上月分别回落47、53 个 PCT;单月销售均价为 1.3 万元/平米,较上月略有提升。1 月公司销售出现短暂下滑,主要是受国内疫情影响,同时恰逢春节销售淡季,销售增速因此出现回落。

拿地稳定,土储质量优良。2020 年 1 月公司单月新增项目 3 例,其中徐州新增项目 1 例,青岛新增项目 2 例,土地建面合计 48.06 万平方米,同比增速-12.46%;新增土地总价 15.26 亿元,同比下降 29.8%。1 月公司拿地均价为 0.32 万元/平,地售比 0.26,维持低位。从新增土储的区域来看,公司新增地块位于徐州睢宁县、青岛即墨区,坚持布局核心区域优质地块。

建筑业务单月合同金额减少,增速明显回升。建筑业务方面,公司 1 月单月获取项目 6 个,预计合同金额 10.7 亿元,较上年同期减少 34%,但增速有所回升,较上月上涨 36%。

投资建议:

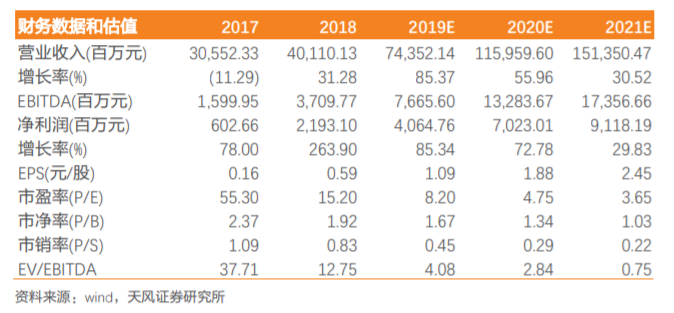

受春节销售淡季与疫情双重影响,公司 1 月销售暂时下滑,预计后续随疫情影响减弱,销量有望逐渐提升,我们认为对于全国大部分区域疫情对居民购房意愿影响较小。如果,此前公司发布业绩预告,2019 年公司归母净利润 39.47 亿元-46.05亿元(对应增速 80%~110%)符合预期,我们认为公司 2020 年兑现业绩承诺仍为大概率事件。回顾 2019 年公司销售增速表现优秀、拿地积极度持续提升,在手土储资源优质,但整体货值偏低,2020 年公司销售增速有望继续保持高增长,但也需要关注新增土储情况,预计公司销售金额有望达到 2400 亿元。我们预计公司19/20 年归母净利润分别为 40.6 亿元、70.2 亿元,对应 EPS 分别为 1.09 元、1.88 元,对应 PE 分别为 8.20X、4.75X,可以看到公司 2020 年对应估值不足 5倍,但业绩有望维持 70%的高速增长,维持“买入”评级。

风险提示:地产政策大幅收紧、房屋价格大幅下跌、疫情防控不及预期

更多精彩內容,請登陸

財華香港網 (https://www.finet.hk/)

現代電視 (http://www.fintv.com)