坚朗五金,一家主营五金配件的公司,2018年底股价尚不足9元,到今年8月中旬飙涨至240元,在短短两年多时间内,股价涨幅超过25倍。从二三十亿元的小公司,成长为了市值最高六七百亿元的行业龙头公司。

然而,这一个多月里,坚朗五金的投资者们却是连连叫苦。自8月达到最高点后,坚朗五金的股价便一路下跌,短短一个月,最低跌至132.55元,跌幅高达44%,市值已经蒸发了近300亿元。

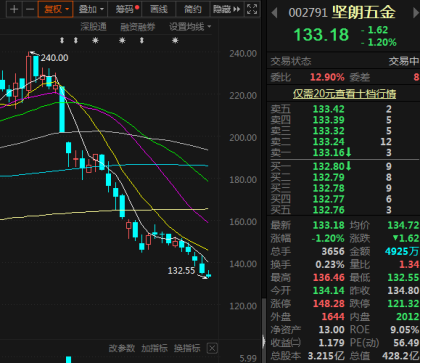

今日开盘,坚朗五金震荡明显,整体仍呈现下行趋势。截至发稿,报价133.18元/股,跌幅1.20%。

股价大跌或因业绩不及预期

近年来,坚朗五金的业绩高速增长,2019年净利润同比增长155%,2020年增长86%。业绩爆发推动了股价的大幅上涨,但估值拔高太多,股价涨幅远超业绩增长。从业绩表现看,过去几年业绩增长4倍出头,但估值却提升了5倍多。

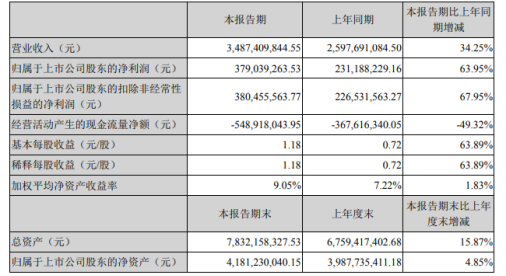

此前8月份,坚朗五金公布了2021年中报,数据显示上半年净利润为3.8亿元,同比增长64%。业绩表现还算不错,但却低于市场预期,导致业绩公布当天公司股价快速跳水,收盘以跌停报收。

据坚朗五金融资融券数据显示,9月16日融资买入590.75万元,融资偿还542.14万元,融资净买入48.61万元,环比减少83.12%。

多家机构表示仍然看好

数据显示,在坚朗五金近期的股价下跌过程中,8月18日以来,共有171家机构参加了坚朗五金的电话会议。

国泰君安表示,公司传统和创新业务均录得较高增长,“研发+制造+服务”全链条模式紧跟市场变化,一站式集成采购产品线持续扩张。上调目标价至222.37元,维持增持评级。

太平洋证券认为,公司目前处于高速成长期,战略定位清晰。给予公司目标价251.5 元,首次覆盖给予“买入”评级。德邦证券、国信证券、中泰证券、东莞证券等多家机构也给出了“买入”评级。

对于近期的业绩表现,坚朗五金表示,地产调控对公司业务有一定影响。从整个产业链上看,受大环境影响,付现比同比也有下降。但公司正在积极开拓海外市场,以快速响应客户供货需求,还在印度、越南、印尼、马来西亚、墨西哥、阿联酋等国家设立了子公司。

更多精彩內容,請登陸

財華香港網 (https://www.finet.hk/)

現代電視 (http://www.fintv.com)